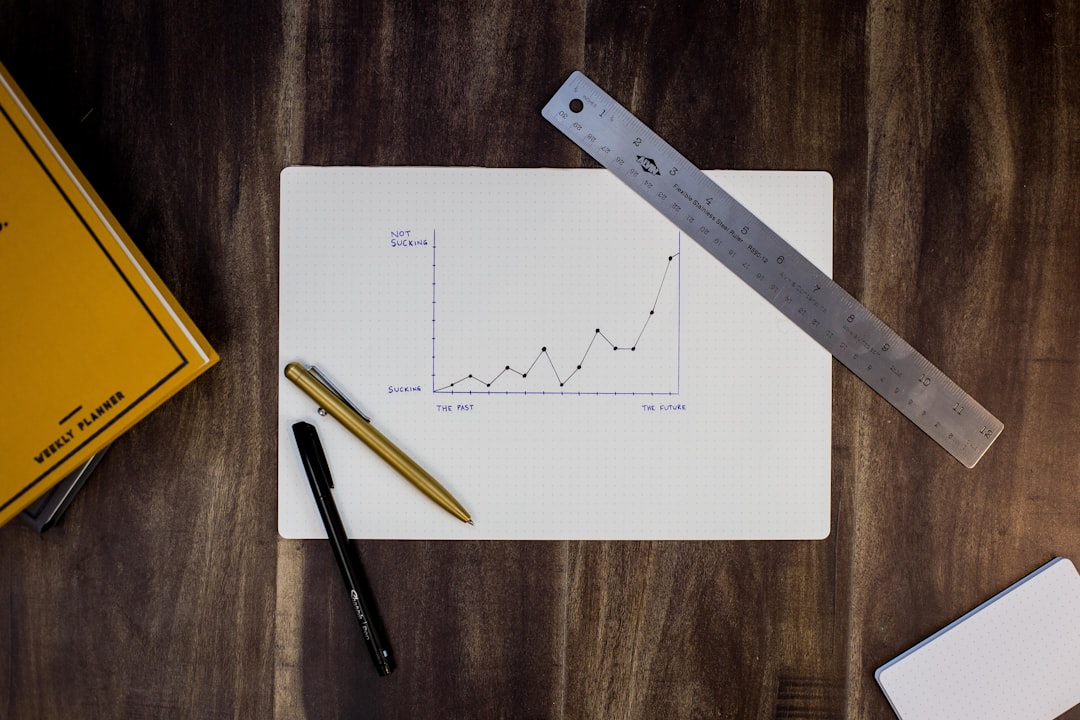

Why Revenge Trading Is Your Worst Enemy (And How to Stop)

You just took a loss. It stings. Your first instinct is to jump back in and win it all back—right now. That feeling is the siren call of revenge trading, and it’s one of the fastest ways to blow up your account. Let’s break down what it is, why it’s so dangerous, and how you can escape its grip.

What Is Revenge Trading?

Revenge trading is when you enter a trade not because of a solid setup, but because you’re angry, frustrated, or desperate after a loss. You want to “get even” with the market. The problem? The market doesn’t care about your feelings. It will punish you again—harder.

Why It’s So Tempting

Losses trigger an emotional response. Your brain releases stress hormones, and your ego screams, “You were right!” So you override your rules, increase your position size, and chase a trade that isn’t there. This is classic cognitive bias in action—specifically the “sunk cost fallacy” and “loss aversion.”

How to Spot Revenge Trading

Look for these red flags in your own behavior:

- You enter a trade immediately after a loss, without waiting for a setup.

- You double or triple your normal position size.

- You ignore your stop-loss or move it wider.

- You feel a knot in your stomach or a rush of anger.

The Simple Setup to Stop It

Here’s a concrete strategy to break the cycle:

1. The 15-Minute Rule: After any loss, step away from your screen for at least 15 minutes. Go walk, drink water, or breathe. This resets your emotional state.

2. The Trade Journal Pause: Before your next trade, write down one sentence: “Why am I taking this trade?” If the answer isn’t a clear, pre-defined setup, don’t enter.

3. Risk a Maximum of 1%: Never risk more than 1% of your account on a single trade, especially after a loss. This caps the damage and keeps you alive.

Risk Management: Your Shield

Risk management isn’t just about stop-losses—it’s about managing your mind. Set a daily loss limit (e.g., 3% of your account). If you hit it, you’re done for the day. No exceptions. This protects you from revenge trading because you physically can’t trade anymore.

Also, use position sizing that makes every loss feel small. If losing a trade makes you anxious, your position is too big. Scale down until you can take a loss without flinching.

The Bottom Line

Revenge trading is a psychological trap, not a strategy. The market will always be there tomorrow. By taking a break, journaling your emotions, and enforcing strict risk limits, you turn a losing habit into a disciplined edge. Remember: the best revenge is a healthy, growing account.

Bitcoin Layer 2s: Stacks, Lightning, and Runes Guide – Scaling Bitcoin for DeFi and Payments

Introduction

Bitcoin, the world’s first and most secure cryptocurrency, has long faced scalability challenges. While its base layer is unmatched in security and decentralization, it processes only a handful of transactions per second. Enter Bitcoin Layer 2 solutions – protocols built on top of Bitcoin that extend its capabilities without compromising its core principles. This guide explores three key Layer 2 innovations: Stacks (for smart contracts and DeFi), Lightning Network (for instant, low-cost payments), and Runes (for efficient token issuance). Whether you’re a developer, investor, or curious user, understanding these layers is essential to navigating the next phase of Bitcoin’s evolution.

Key Concepts

1. Stacks (STX) – Smart Contracts for Bitcoin

Stacks is a Layer 1 blockchain that connects to Bitcoin via a unique mechanism called Proof of Transfer (PoX). It enables smart contracts and decentralized applications (dApps) while anchoring its security to Bitcoin’s hash power. Key features include:

- Clarity Smart Contracts: A predictable, decidable language that prevents reentrancy attacks.

- Bitcoin-Backed Assets: sBTC, a 1:1 Bitcoin peg, allows Bitcoin to be used in DeFi on Stacks.

- Nakamoto Upgrade: Faster block times (5 seconds) and improved finality.

2. Lightning Network – Instant, Scalable Payments

The Lightning Network is a second-layer payment protocol that operates on top of Bitcoin. It creates a network of payment channels, enabling near-instant transactions with minimal fees. Core concepts:

- Payment Channels: Two parties lock funds in a multi-signature address and transact off-chain.

- HTLCs (Hashed Time-Locked Contracts): Enable trustless routing across multiple channels.

- Wumbo Channels: Larger channel capacities for high-volume use cases.

3. Runes – Efficient Token Protocol

Runes is a new token standard on Bitcoin that allows users to create and transfer fungible tokens directly on the Bitcoin blockchain. Unlike BRC-20 (which uses Ordinals), Runes is designed for efficiency and simplicity:

- UTXO-Based: Tokens are stored in Bitcoin’s UTXO model, reducing blockchain bloat.

- No Native Token: No need for a separate token to pay fees – uses Bitcoin for gas.

- Mint and Transfer: Simple operations that leverage Bitcoin’s security.

Pro Tips

- Start Small with Lightning: Use wallets like Phoenix or Breez to test small payments before committing large amounts.

- Stack STX for Rewards: Stacking STX tokens earns Bitcoin rewards via PoX – a great way to earn passive income.

- Monitor Runes Projects: Runes are new; stick to audited projects and avoid FOMO on unverified mints.

- Use a Hardware Wallet: For long-term holdings of sBTC or STX, store them on a Ledger or Trezor.

FAQ Section

Q: Are Bitcoin Layer 2s safe?

A: Yes, but each has different security models. Lightning relies on channel monitoring, Stacks uses Bitcoin finality, and Runes inherits Bitcoin’s security. Always use reputable wallets and services.

Q: Can I use Bitcoin directly on Stacks?

A: Yes, via sBTC – a 1:1 Bitcoin-backed asset that can be used in DeFi protocols on Stacks.

Q: What is the difference between Runes and BRC-20?

A: Runes is UTXO-based and more efficient than BRC-20 (which uses Ordinals inscriptions). Runes reduces blockchain bloat and is simpler to implement.

Q: Do I need to run a node to use Lightning?

A: No. Non-custodial wallets like Phoenix or Breez handle channel management automatically. For advanced users, running a node (e.g., LND) offers more control.

Q: How do I earn rewards on Stacks?

A: By stacking STX tokens. You delegate STX to a stacking pool or run your own node to earn Bitcoin rewards.

Conclusion

Bitcoin Layer 2s are unlocking new possibilities for the world’s most secure blockchain. Stacks brings smart contracts and DeFi, Lightning enables instant global payments, and Runes offers efficient tokenization. Each solution addresses a specific limitation while preserving Bitcoin’s core values. As these technologies mature, they will drive the next wave of Bitcoin adoption – from microtransactions to decentralized finance. For more details on this, check out our guide on Restaking Explained: EigenLayer and Beyond | Complete Guide 2024. You might also be interested in reading about The VWAP Day Trading Strategy: Your Guide to Trading with the ‘Smart Money’.

Onchain Privacy and Accountability: How They Can Coexist, Explained

Can crypto transactions be both private and compliant? That question has divided the blockchain world for years. But according to experts at Consensus Miami 2026, the answer is a clear “yes.” Panelists from Moody’s Ratings and ChangeNOW argued that hybrid blockchain architecture and address-level monitoring can solve the privacy-accountability tension without sacrificing either goal. For crypto users navigating increasingly complex regulations, understanding this balance is crucial. This guide breaks down how onchain privacy and accountability can work together, the technology making it possible, and what it means for your transactions in 2025.

Read time: 9-11 minutes

Understanding Onchain Privacy and Accountability for Beginners

Onchain privacy refers to a user’s ability to transact on a public blockchain without exposing their real-world identity, while accountability means that transactions can still be traced and audited when necessary. Think of it like a post office box versus a home address. A PO box lets you receive mail without revealing where you live (privacy), but postal inspectors can still trace illegal packages through their tracking numbers if needed (accountability). Public blockchains like Bitcoin and Ethereum make every transaction visible to anyone, but that transparency historically came at the cost of user privacy—anyone could link your wallet address to your identity if you weren’t careful.

Why did this tension arise? Crypto’s original promise was the ability to transact without trusted intermediaries or personal identification. But as institutions entered the space, regulators demanded the same anti-money laundering (AML) and know-your-customer (KYC) standards found in traditional finance. The core question became: can you have Bitcoin’s pseudonymity while also satisfying compliance requirements?

A real-world example: ChangeNOW, a non-custodial exchange, lets users swap cryptocurrencies without mandatory KYC. But when law enforcement asks about suspicious funds, the company can trace which wallet addresses moved the money without revealing who owns those addresses. This is the coexistence model in action.

The Technical Details: How an Onchain Intelligence Layer Works

Panelists at Consensus Miami described an emerging “intelligence layer” that splits accountability work across different parts of the blockchain ecosystem. Here’s how it functions:

1. Hybrid Blockchain Architecture: Networks are divided into two types. Private permissioned blockchains handle sensitive institutional transactions with verified participants. Public permissionless chains like Bitcoin or Ethereum provide liquidity and open access. The two connect through bridges or sidechains.

2. Wallet-Address-Level Monitoring: Instead of identifying real-world identities (names, addresses, social security numbers), compliance tools track wallet addresses. This creates a pseudonymous trail that can be monitored for suspicious patterns without automatically doxxing users.

3. Blockchain Forensics Integration: Platforms use tools from firms like Chainalysis or CipherTrace to screen transactions against known illicit addresses (sanctions lists, darknet markets, hack proceeds) in real time.

4. Selective Disclosure: When authorities provide valid legal requests, platforms can share transaction data associated with specific addresses—but only the addresses, not the person behind them.

Why this structure matters for you: It means you can potentially use non-custodial services without uploading your passport, while still allowing legitimate law enforcement to pursue criminals. Your privacy isn’t absolute—but it’s much stronger than handing over your ID for every swap.

Current Market Context: Why This Matters Now

The push for onchain privacy with accountability comes at a critical moment for crypto adoption. According to Rajeev Bamra, global head of strategy for digital economy at Moody’s Ratings, institutional digital finance has grown by “over 100 or 150%” in the past 18 months. However, at roughly $35 billion, it remains a tiny fraction of the $200 trillion-plus in traditional clearing flows handled annually by conventional finance.

This gap explains why institutions demand accountability. Without it, they can’t enter the space at scale. The panel highlighted two key regulatory frameworks driving change:

- Europe’s Markets in Crypto-Assets Regulation (MiCA): Requires clear rules around asset quality, segregation, and liability for stablecoin issuers and crypto service providers.

- The U.S. GENIUS Act: A proposed framework asking similar fundamental questions about custody, capital requirements, and consumer protection.

Bamra noted that while these frameworks share “regulatory convergence in intention,” they diverge sharply in execution. This fragmentation creates complexity for platforms trying to serve global users while maintaining privacy.

Competitive Landscape: How Different Approaches Compare

| Feature | Traditional Finance (KYC/AML) | ChangeNOW Model | Fully Anonymous Chains (Monero) |

|---|---|---|---|

| User Identity Required | Yes (name, address, ID) | No (wallet address only) | No |

| Transaction Traceability | Full (bank records) | Address-level mapping | Extremely difficult |

| Compliance Readiness | High (regulated banks) | Medium (works with AML providers) | Low (often blocked by exchanges) |

| Privacy Level | Minimal | Strong pseudonymity | Near-total |

| Institutional Adoption | Established | Emerging | Very limited |

| Regulatory Risk for Users | Low (compliant) | Moderate | High (many exchanges won’t list) |

Why this matters: The ChangeNOW approach occupies a middle ground that may appeal to users who want more privacy than Coinbase offers but don’t need the full anonymity of privacy coins like Monero, which many regulated platforms now avoid.

Practical Applications: Real-World Use Cases

How does onchain privacy with accountability work in practice?

- Registration-Free Swaps: Platforms like ChangeNOW let you exchange cryptocurrencies without creating an account or uploading ID. Your transaction is screened against illicit addresses, but your identity stays private.

- Institutional Custody for High-Net-Worth Individuals: Private permissioned networks allow wealthy investors to hold digital assets with institutional-grade oversight while keeping their personal details off public blockchains.

- Regulatory Reporting for Exchanges: When authorities request data, exchanges can provide wallet-level transaction records without revealing customer identities—fulfilling compliance obligations while respecting privacy.

- Cross-Border Payments for Businesses: Companies can send large value transfers through hybrid networks that verify counterparties on private chains while settling final transactions on public chains for liquidity.

- DeFi Lending with Credit Scoring: Imagine a DeFi protocol that assesses your creditworthiness based on your wallet’s history without requiring you to reveal your name or address.

Risk Analysis: Expert Perspective

Primary Risks:

1. Privacy Erosion: Address-level monitoring could eventually be combined with other data sources (IP addresses, exchange records) to de-anonymize users. The line between “address mapping” and “identity mapping” is thin.

2. Regulatory Creep: What starts as selective disclosure could expand into mandatory identity requirements, especially if regulators push for travel rule compliance on all transactions.

3. Technical Complexity: Hybrid architectures require careful engineering. Bridge vulnerabilities have led to hundreds of millions in losses (e.g., the $600 million Ronin bridge hack).

Mitigation Strategies:

- Use Multiple Wallets: Separate funds across different wallets for different purposes (trading, savings, privacy-sensitive transactions) to reduce correlation risks.

- Choose Platforms Transparent About Compliance: Look for services that clearly explain what data they share with authorities and under what circumstances.

- Monitor Regulatory Developments: Frameworks like MiCA and the GENIUS Act are still evolving. Understanding your jurisdiction’s rules helps you make informed choices.

Expert Consensus: Pauline Shangett, chief strategy officer at ChangeNOW, framed the debate as a liability issue: “The agents who should be held liable for the regulatory frameworks are agents who are dealing with emission and not transmission.” In other words, responsibility should fall on issuers and platforms, not users who are simply moving funds.

Beginner’s Corner: Quick Start Guide

If you want to preserve privacy while staying compliant, here’s how to start:

1. Understand Wallet Basics: Learn the difference between custodial wallets (exchange-controlled) and non-custodial wallets (you control the keys). Non-custodial wallets offer more privacy.

2. Choose a Non-KYC Exchange for Small Swaps: Platforms like ChangeNOW let you swap small amounts without ID. For larger amounts, you may need KYC.

3. Use a Privacy-Focused Wallet: Consider wallets like Wasabi (Bitcoin) or Railgun (Ethereum) that implement coinjoins or zero-knowledge proofs for enhanced privacy.

4. Layer 2 Solutions: Moving funds to Layer 2 networks (Lightning Network, Arbitrum) can reduce onchain footprint and improve privacy.

5. Avoid Mixers Without Research: Traditional mixing services have been shut down or compromised. If you use one, understand the legal risks in your jurisdiction.

Common Mistake to Avoid: Assuming that address-level monitoring means no one can ever identify you. If you fund your wallet from a centralized exchange with KYC, your identity is already linked to that address.

Future Outlook: What’s Next

The road ahead for onchain privacy and accountability includes:

1. Regulatory Convergence: While fragmentation exists today, expect gradual harmonization as major economies (EU, US, UK, Japan) align basic compliance standards.

2. Zero-Knowledge Proofs (ZKPs): Technologies like zk-SNARKs can prove a transaction is valid without revealing transaction details. This could allow full compliance without any privacy sacrifice.

3. Institutional Lobbying: As the $35 billion institutional market grows, expect stronger industry efforts to shape regulations that favor hybrid privacy solutions over blanket KYC mandates.

4. Self-Sovereign Identity (SSI): Users may soon hold their own credentials (verified by attestors) and selectively disclose them to platforms without uploading IDs to centralized databases.

The panel’s core message is that privacy and accountability aren’t mutually exclusive—they’re design choices. The winning platforms will be those that balance both effectively, giving users control over their data while satisfying legitimate compliance needs.

Key Takeaways

- Onchain privacy and institutional accountability can coexist through hybrid blockchain architecture and address-level monitoring that doesn’t require revealing real-world identities by default.

- Address-level monitoring maps wallet addresses, not people, allowing compliance with law enforcement requests without doxxing users.

- Regulatory convergence is happening in intention but not yet in execution, creating complexity for global platforms.

- Users can take practical steps today to preserve privacy, including using non-KYC services for small transactions and separating wallets by purpose.

,

“datePublished”: “2026-05-08T00:01:42.053-04:00”,

“dateModified”: “2026-05-08T00:01:42.053-04:00”,

“mainEntity”: {

“@type”: “Thing”,

“name”: “Onchain Privacy and Accountability”

}

}

How to Secure Your Crypto Wallet: A Step-by-Step Guide

Introduction

In the world of cryptocurrency, security is paramount. With billions of dollars lost annually to hacks, phishing scams, and user errors, knowing how to properly secure your crypto wallet is not optional—it’s essential. Whether you’re a beginner or a seasoned trader, this step-by-step guide will walk you through the best practices to protect your digital assets from theft, loss, and unauthorized access.

Key Concepts

- Private Keys vs. Seed Phrases: Your private key is like a password that proves ownership of your funds. A seed phrase (usually 12 or 24 words) is a backup that can restore your wallet. Never share either with anyone.

- Hot Wallets vs. Cold Wallets: Hot wallets are connected to the internet (e.g., mobile apps, browser extensions) and are convenient but more vulnerable. Cold wallets (hardware wallets, paper wallets) are offline and much more secure for long-term storage.

- Two-Factor Authentication (2FA): Adds an extra layer of security by requiring a second verification method (like Google Authenticator or a hardware key) beyond your password.

- Phishing Attacks: Fake websites, emails, or messages that trick you into revealing your private keys or seed phrase. Always double-check URLs and never click suspicious links.

Pro Tips

- Use a hardware wallet for large holdings. Devices like Ledger or Trezor keep your private keys offline.

- Enable 2FA on every exchange and wallet. Prefer authenticator apps over SMS-based 2FA.

- Write down your seed phrase on paper and store it in a safe place (e.g., a fireproof safe). Never store it digitally.

- Keep your software updated. Wallet apps and browser extensions often release security patches.

- Use a dedicated device or browser profile for crypto transactions to minimize exposure to malware.

💡 Pro Tip

Looking for altcoin opportunities and smooth trading? Try KuCoin.

FAQ Section

1. What is the safest type of crypto wallet?

Hardware wallets (cold wallets) are considered the safest because they store your private keys offline, making them immune to online hacks.

2. Can I recover my wallet if I lose my phone?

Yes, if you have your seed phrase. Simply download the same wallet app on a new device and enter your seed phrase to restore access.

3. Is it safe to keep crypto on an exchange?

Exchanges are convenient for trading, but they are more vulnerable to hacks. For long-term storage, transfer your funds to a private wallet, preferably a hardware wallet.

4. What should I do if I think my wallet is compromised?

Immediately transfer your funds to a new wallet with a new seed phrase. Revoke any token approvals and change passwords on all related accounts.

5. How often should I update my wallet software?

As soon as updates are released. Enable automatic updates if possible, and always download updates from the official source.

Conclusion

Securing your crypto wallet is a continuous process, not a one-time setup. By following the steps in this guide—using cold storage, enabling 2FA, safeguarding your seed phrase, and staying vigilant against phishing—you can dramatically reduce the risk of losing your assets. Remember: in crypto, you are your own bank. Take that responsibility seriously.

For more details on this, check out our guide on The Bollinger Band Squeeze: Your Signal for the Next Big Move.

You might also be interested in reading about DePIN Explained: Earning Passive Income with Infrastructure.

US Treasury Bills on Blockchain: The Risk-Free Rate On-Chain

Introduction

US Treasury Bills (T-Bills) are short-term debt obligations issued by the U.S. Department of the Treasury, widely regarded as the closest proxy to a ‘risk-free’ asset in global finance. Traditionally, these instruments are traded over-the-counter (OTC) or through brokerage accounts, with settlement cycles of T+1 or T+2 and limited accessibility for retail investors. Tokenization brings T-Bills on-chain, enabling fractional ownership, 24/7 liquidity, and transparent, programmable settlement. Off-chain T-Bills require intermediaries, minimum investment sizes (often $1,000 or more), and are subject to market hours. On-chain T-Bills are represented as ERC-20 or similar tokens, each backed 1:1 by an underlying T-Bill held in a Special Purpose Vehicle (SPV). This allows investors to buy, sell, or use T-Bill tokens as collateral in DeFi protocols at any time, with near-instant settlement.

How It Works

The tokenization of US Treasury Bills follows a structured process that bridges traditional custody with blockchain transparency:

- Tokenization: A regulated issuer (e.g., Ondo Finance, Backed Finance) creates a token representing a fractional interest in a pool of T-Bills. Each token is typically pegged to $1 or a fixed notional value.

- Special Purpose Vehicle (SPV): The issuer establishes an SPV that holds the actual T-Bills in a segregated custody account with a qualified custodian (e.g., a bank or broker-dealer). The SPV ensures legal separation between the issuer’s assets and the token holders’ assets.

- Oracle Integration: A trusted oracle (e.g., Chainlink, Pyth) feeds the net asset value (NAV) of the T-Bill portfolio on-chain. This price is updated periodically (e.g., daily) to reflect accrued interest and market value.

- Blockchain Minting/Burning: When an investor deposits fiat or stablecoins, the issuer mints new tokens and credits them to the investor’s wallet. Upon redemption, tokens are burned, and the equivalent fiat is returned. Smart contracts automate the minting/burning process based on oracle-verified NAV.

- Secondary Market: Tokenized T-Bills can be traded on decentralized exchanges (DEXs) or centralized platforms, providing 24/7 liquidity. Some protocols also allow using these tokens as collateral for lending or yield farming.

Investment Analysis

Pros

- Fractional Ownership: Low minimum investment (e.g., $1 tokenized) opens T-Bill exposure to retail investors globally.

- 24/7 Liquidity: On-chain trading eliminates market hours, allowing instant swaps and portfolio rebalancing.

- Transparency: All transactions are recorded on a public ledger, with NAV updates verifiable via oracles.

- Programmability: Tokens can be integrated into DeFi protocols for lending, borrowing, or as collateral, generating additional yield.

- Regulatory Clarity: T-Bills are exempt from SEC registration under certain exemptions (e.g., Regulation D), and issuers often comply with KYC/AML requirements.

Cons

- Counterparty Risk: Investors rely on the issuer and custodian to hold the underlying T-Bills. If the issuer becomes insolvent, token holders may face delays in redemption.

- Smart Contract Risk: Bugs or exploits in the token contract or oracle can lead to loss of funds.

- Regulatory Uncertainty: While T-Bills themselves are low-risk, the tokenization framework may face evolving regulations from the SEC, CFTC, or state regulators.

- Oracle Dependency: If the oracle fails or provides stale data, the token price may deviate from NAV, causing arbitrage or liquidation risks.

- Limited Yield: T-Bill yields are currently modest (4-5% APY), which may be lower than some DeFi yields, though with significantly lower risk.

Risks

- Regulatory Risk: Future rules could classify tokenized T-Bills as securities, requiring registration or limiting secondary trading.

- Liquidity Risk: In stressed markets, the secondary market for tokenized T-Bills may dry up, forcing holders to rely on the issuer’s redemption process (which may have delays).

- Custodial Risk: The SPV’s custodian must be trusted; any failure (e.g., bankruptcy) could affect the underlying assets.

- Smart Contract Risk: Code vulnerabilities can lead to theft or permanent loss of tokens.

For a broader market view, check out our analysis on Etherscan Guide: Track Whales & Verify Transactions.

Investors often compare this to Cold Storage vs Hot Wallets: Which Should You Choose? A Complete Guide for Crypto Security.

Tool Recommendation

Looking for altcoin opportunities and smooth trading? Try KuCoin. KuCoin offers a wide range of tokenized assets, including RWA tokens, and provides a user-friendly interface for both spot and margin trading. Whether you’re a beginner or an experienced trader, KuCoin’s advanced tools and liquidity make it a solid choice for accessing on-chain T-Bill products and other DeFi instruments.

FAQ Section

What is the yield on tokenized US Treasury Bills?

The yield on tokenized T-Bills typically mirrors the yield of the underlying Treasury Bills, minus management fees charged by the issuer (usually 0.15% to 0.50% annually). As of early 2025, yields range from 4.0% to 5.0% APY, depending on the duration of the T-Bills held in the pool.

Are tokenized T-Bills considered securities?

Yes, in most jurisdictions, tokenized T-Bills are classified as securities because they represent an investment in a common enterprise with an expectation of profit derived from the efforts of others. Issuers often rely on exemptions like Regulation D (accredited investors) or Regulation S (non-US investors) to avoid full SEC registration. Investors should verify the regulatory status in their jurisdiction.

How do I redeem tokenized T-Bills for fiat?

Redemption processes vary by issuer. Typically, you send the tokens back to the issuer’s smart contract or a designated redemption address. The issuer then burns the tokens and sends the equivalent fiat (or stablecoins) to your bank account or wallet. Redemption may take 1-5 business days, depending on the issuer’s liquidity and banking relationships.

Conclusion

Tokenized US Treasury Bills represent a significant bridge between TradFi and DeFi, offering a low-risk, yield-bearing asset that is accessible 24/7 and programmable for DeFi use. While the asset class carries counterparty, regulatory, and smart contract risks, the underlying T-Bills remain one of the safest investments globally. For institutional and accredited investors, tokenized T-Bills provide a compliant way to earn yield on idle cash while maintaining liquidity. For retail investors, fractional ownership lowers the barrier to entry. As the RWA ecosystem matures, on-chain T-Bills are likely to become a core component of diversified crypto portfolios. However, due diligence on the issuer, custodian, and smart contract audits is essential before investing.

Animoca Brands Chairman Declares Metaverse Over, Predicts 100 Billion AI Agents

May 22, 2026 — Animoca Brands chairman Yat Siu announced at Consensus Miami 2026 that the metaverse, as originally envisioned during the pandemic, is dead as a consumer destination. Siu instead predicted 50 to 100 billion AI agents will become blockchain’s primary users, vastly outnumbering human cryptocurrency participants.

Immediate Details & Direct Quotes

Want to trade this news? Bitget offers professional charting tools and deep liquidity.

Siu told the Consensus Miami 2026 conference on Thursday that the blockchain-based metaverse was never truly designed for human consumers. “Where we’re landing is that the metaverse, the blockchain-based one, was really the proof of concept for agents,” he said. “In other words, it was never really destined for humans as a prime consumer.”

The remarks represent a significant pivot for Animoca Brands, which was among the most vocal proponents of the pandemic-era vision where users would spend increasing amounts of their social and economic lives in immersive virtual environments. Siu attributed the earlier misconception to COVID-19 lockdown conditions, when many assumed remote digital life would become permanent.

“Everyone thought, ‘Oh, we’re going to be at home, and we’re never going to travel as much anymore,'” Siu recalled. “Which, of course, turned out to be quite the opposite.”

As part of the strategic shift, Animoca announced a $10 million investment initiative for developers building AI agent applications through its Animoca Minds platform, framing autonomous agents as the firm’s next major investment category following the metaverse era.

Market Context & Reaction

Siu’s new thesis centers on blockchain technology becoming the financial infrastructure for machine-to-machine transactions. “Blockchain technology is the ideal financial system for machines,” he said. “We, the humans, were basically the guinea pigs.”

The argument addresses a persistent challenge limiting crypto adoption. According to industry data cited by Siu, approximately 700 to 800 million people globally own some form of cryptocurrency, yet fewer than 70 million actively use blockchain applications. The technology remains too complex for mainstream consumers—a barrier AI agents don’t face.

Agents interact directly through code, require no traditional banking infrastructure, and can transact autonomously on-chain. Siu estimates 50 to 100 billion AI agents could eventually operate on the internet. Based on current global population math, that translates to 10 to 20 agents per human, producing between 70 and 140 billion agents worldwide.

“I think the point is that it’s going to be more agents than humans,” Siu stated.

Background & Historical Context

Animoca Brands built its reputation as a leading metaverse advocate during the pandemic. The Hong Kong-based software and venture capital firm invested heavily in blockchain gaming, digital land, and virtual world infrastructure, positioning itself at the center of the Web3 metaverse movement.

The company’s portfolio includes investments in The Sandbox, Decentraland, and other virtual world projects that attracted billions in speculation during 2021 and early 2022. The metaverse concept drove significant capital inflows, with major brands and celebrities purchasing virtual real estate and launching digital experiences.

However, user engagement metrics never matched the hype. Most virtual worlds saw declining active users after lockdowns ended, as consumers returned to physical travel and in-person social activities. The disconnect between speculation and actual usage has forced metaverse-focused companies to reassess their strategies.

What This Means

In the short term, Animoca’s pivot signals a potential industry-wide shift away from consumer metaverse narratives toward AI agent infrastructure. The $10 million Animoca Minds investment initiative will likely accelerate development of autonomous agent applications on blockchain networks.

Long-term implications suggest blockchain networks may prioritize machine-to-machine transactions over human user interfaces. This could fundamentally change how crypto projects design their products, shifting focus from user experience improvements toward agent-compatible protocols and smart contract standards.

For investors and developers, the announcement suggests opportunities may lie in building agent infrastructure, including identity systems, payment channels, and autonomous transaction protocols, rather than consumer-facing metaverse applications.

—

The Rise of AI Agents in Crypto: A Complete Guide

Introduction

Artificial Intelligence (AI) agents are rapidly transforming the cryptocurrency landscape, automating trading, portfolio management, and even governance. These autonomous programs analyze vast amounts of data, execute trades, and interact with blockchain protocols without human intervention. As the crypto market matures, AI agents are becoming essential tools for both retail and institutional investors seeking efficiency, speed, and data-driven decision-making. This guide explores the key concepts, practical tips, and tools you need to understand and leverage AI agents in crypto.

Key Concepts

- Autonomous Trading Bots: AI agents that execute trades based on predefined strategies, market sentiment analysis, or machine learning models. They can operate 24/7 and react to market changes in milliseconds.

- DeFi Integration: AI agents can interact with decentralized finance protocols to automate yield farming, liquidity provision, and arbitrage opportunities, optimizing returns while minimizing risk.

- On-Chain Analytics: Agents analyze blockchain data (e.g., transaction volumes, wallet activity, smart contract interactions) to identify trends, detect anomalies, and predict price movements.

- Governance Automation: In DAOs, AI agents can vote on proposals based on predefined criteria, ensuring consistent participation and reducing manual oversight.

- Risk Management: AI agents can monitor portfolio exposure, set stop-losses, and rebalance assets automatically to protect against market volatility.

Pro Tips

- Start with a clear strategy: Define your goals (e.g., arbitrage, long-term holding, yield farming) before deploying an AI agent. Backtest your strategy using historical data.

- Monitor performance regularly: Even autonomous agents need oversight. Set up alerts for unusual behavior or significant drawdowns.

- Optimize for low fees: High transaction costs can erode profits, especially for high-frequency strategies. Choose exchanges with competitive fee structures.

- Use multiple data sources: Combine on-chain data, social media sentiment, and market indicators to improve your agent’s accuracy.

- Security first: Only grant minimal permissions to your AI agent. Use hardware wallets and avoid sharing private keys.

FAQ Section

What are AI agents in crypto?

AI agents are autonomous software programs that use machine learning and data analysis to perform tasks like trading, portfolio management, and governance in the cryptocurrency space.

Are AI agents safe to use?

Safety depends on the implementation. Use reputable platforms, limit permissions, and regularly audit your agent’s activity. Never share private keys.

Can AI agents guarantee profits?

No. While AI agents can improve efficiency and reduce emotional bias, they are not foolproof and can still incur losses, especially in volatile markets.

Do I need coding skills to use an AI agent?

Many platforms offer no-code interfaces for deploying AI agents. However, custom strategies may require basic programming knowledge.

What is the best exchange for AI agent trading?

Exchanges with low fees, high liquidity, and robust APIs are ideal. MEXC is a popular choice due to its competitive fee structure and support for automated trading.

Conclusion

AI agents are revolutionizing the crypto industry by automating complex tasks, improving efficiency, and enabling data-driven strategies. Whether you are a seasoned trader or a newcomer, integrating AI agents into your workflow can provide a significant edge. Start with a clear plan, prioritize security, and always keep an eye on costs. For more details on this, check out our guide on Israeli Regulators Approve Shekel-Pegged Stablecoin. You might also be interested in reading about Stablecoin Yield Strategies: Low Risk Farming – A Comprehensive Guide.

Bridging Worlds: How Real World Asset Tokenization is Changing Crypto Trading

Imagine being able to trade a fraction of a Manhattan skyscraper, a barrel of premium crude oil, or even a rare vintage car – all from your phone, 24/7, with the speed and transparency of blockchain. This isn’t science fiction; it’s the reality of Real World Asset (RWA) tokenization. For traders, this represents one of the most exciting and foundational shifts in the market today. It’s not just another DeFi trend; it’s a bridge between the trillion-dollar traditional finance world and the digital frontier.

How it Works

At its core, RWA tokenization is the process of converting the ownership rights of a physical or traditional financial asset into a digital token on a blockchain. Think of it like a digital deed. Instead of buying a whole bond or a piece of real estate, you can buy a token that represents a share of that asset. This token lives on a public ledger, making it transparent, easily divisible, and tradeable.

The Setup: Why Traders Should Pay Attention

For the crypto trader, RWA tokens offer unique opportunities that differ from trading volatile cryptocurrencies like Bitcoin or memecoins. Here’s the setup:

1. Yield from Stability: Many RWA tokens are designed to generate yield from real-world income, such as rent from properties or interest from loans. This provides a stable, predictable return stream that can act as a hedge during volatile crypto market cycles.

2. Diversification: By trading RWAs, you gain exposure to asset classes that historically have low correlation with crypto. This can smooth out your overall portfolio performance.

3. Arbitrage Opportunities: As this sector is still nascent, price inefficiencies often exist between the tokenized asset and its underlying real-world value. Savvy traders can capitalize on these spreads.

4. On-Chain Transparency: You can verify the underlying asset and its performance through on-chain data and governance, reducing the opacity often found in traditional finance.

Risk Management

While exciting, RWA trading isn’t without its risks, and managing them is crucial:

- Counterparty Risk: The value of the token is only as good as the entity managing the underlying asset. Always research the issuer, their legal structure, and their track record.

- Oracle Risk: RWAs rely on oracles to bring off-chain data (like property appraisals or interest rates) onto the blockchain. A compromised or inaccurate oracle can break the peg.

- Liquidity Risk: Some RWA tokens may have low trading volume, making it difficult to exit a position quickly without slippage. Stick to tokens on established platforms with decent liquidity.

- Regulatory Risk: The legal classification of tokenized assets is still evolving globally. A sudden regulatory change could impact the token’s tradability or value.

Pro Tip: Start small. Allocate only a small percentage of your trading capital (e.g., 5-10%) to RWAs while you learn the ropes. Focus on tokens that have undergone third-party audits and have a clear legal framework for the underlying asset.

Conclusion

Real World Asset tokenization is more than a narrative; it’s the next logical step in the maturation of crypto markets. For the beginner and intermediate trader, it offers a unique path to combine the efficiency of DeFi with the stability of traditional finance. By understanding the setup and respecting the risks, you can position yourself at the forefront of this transformative trend. The bridge between the real world and the digital world is open – are you ready to cross?

How Stablecoin Compliance Works: A Beginner’s Guide to Coinbax’s Programmable Escrow

Did you know that stablecoins now settle over $1 trillion in transactions monthly? As banks rush to use stablecoins for payments, they face a critical challenge: how to maintain regulatory compliance when funds move directly between crypto wallets. This is exactly what startup Coinbax aims to solve. The company recently won the $20,000 grand prize at Consensus Miami’s PitchFest for its programmable escrow system that adds compliance controls to onchain payments. For crypto users and financial institutions alike, understanding how compliance can work on blockchain rails is essential for the future of digital payments. This guide explains Coinbax’s innovation in plain language, shows how banks are adopting stablecoins safely, and clarifies common misconceptions about onchain compliance.

Read time: 10-12 minutes

Understanding Stablecoin Compliance for Beginners

Stablecoin compliance refers to the processes and technologies that ensure cryptocurrency transactions involving stablecoins meet legal and regulatory requirements. Think of it like a digital security checkpoint at an airport—every passenger (transaction) must show valid ID, pass through screening, and get clearance before boarding (settling on the blockchain).

Why was this created? Traditional bank transfers already have built-in compliance checks because banks act as intermediaries who verify identities, screen for sanctions, and assess transaction risk. However, when stablecoins move directly between wallets on a blockchain, these checks don’t happen automatically. This creates a problem for banks that want to use stablecoins for faster, cheaper payments but need to satisfy their compliance departments.

A real-world example: Imagine Bank A wants to send $1 million in USDC (a popular stablecoin) to Bank B. Without Coinbax’s system, the transaction goes directly from one wallet to another with no built-in compliance checks. With Coinbax’s programmable escrow, the funds are held temporarily while third-party services verify identities, check sanctions lists, and assess risk—only then does the payment settle onchain.

The Technical Details: How Coinbax’s Programmable Escrow Actually Works

Coinbax uses smart contracts—self-executing code on a blockchain—to create a trust layer for stablecoin payments. Here’s how the system operates:

1. Escrow Creation: When a bank initiates a stablecoin payment, the funds are first moved into a smart contract that acts as a digital escrow account. The smart contract holds the funds temporarily and won’t release them until conditions are met.

2. Compliance Verification: Third-party services are called by the smart contract to perform three key checks:

– Identity verification: Confirming the sender and receiver are who they claim to be

– Sanctions screening: Checking against global sanctions lists (like OFAC)

– Transaction risk assessment: Evaluating whether the payment amount or pattern looks suspicious

3. Conditional Settlement: Only after all compliance checks pass do the smart contracts automatically release the funds to the intended recipient. If any check fails, the transaction is blocked and funds return to the sender.

4. Blockchain Recording: The entire compliance process is recorded on the blockchain, creating an immutable audit trail that regulators can review.

Why this structure matters for you: This system allows banks to benefit from stablecoin’s speed and low cost while maintaining the same compliance standards they use for traditional wire transfers. For users, it means faster international payments without sacrificing security.

Visual Cue: A flow diagram showing the transaction path from Bank A → Escrow Smart Contract → Compliance Checks → Conditional Settlement → Bank B would help visualize this process.

Current Market Context: Why This Matters Now

Stablecoins are experiencing explosive growth. According to CoinGecko, the total stablecoin market cap exceeded $200 billion in late 2025, with daily transaction volumes regularly surpassing $100 billion. Major financial institutions are taking notice.

Coinbax’s founder, Peter Glyman, a former executive at Jack Henry (a major banking technology provider), launched the startup in October 2025. Within just two months, the company closed a seed round and went live on Base mainnet—Coinbase’s Layer 2 blockchain built on Ethereum. The company is already running pilot programs with banks, custody firms, and wallet providers.

The timing is significant for several reasons:

- Regulatory clarity: The EU’s Markets in Crypto-Assets (MiCA) regulation, which took full effect in 2025, provides a clear framework for stablecoin issuance and compliance

- Institutional adoption: Bridge and Deus X Capital executives recently stated at Consensus 2026 that large corporations are actively exploring stablecoins for cross-border treasury payments

- AI integration: Stablecoin rails are enabling AI agents to make autonomous micropayments, creating new use cases that require robust compliance controls

Competitive Landscape: How Coinbax Compares

Several companies are working on stablecoin compliance solutions, each with different approaches:

| Feature | Coinbax | Traditional Banking Rails | Decentralized Compliance Protocols |

|---|---|---|---|

| Transaction Speed | Near-instant (seconds) | 1-3 business days | Near-instant |

| Compliance Location | Onchain (smart contract) | Offchain (bank systems) | Onchain (automated) |

| Cost per Transaction | <$0.01 | $15-$50+ | <$0.01 |

| Regulatory Oversight | Full (bank-grade checks) | Full (existing systems) | Variable |

| User Control | Bank-managed wallets | Bank-managed accounts | Self-custody wallets |

| Key Innovation | Programmable escrow | Mature infrastructure | Automated rule execution |

Why this matters for users: Coinbax distinguishes itself by bridging the gap between traditional banking compliance and decentralized blockchain technology. Unlike fully decentralized solutions that may struggle with regulatory requirements, or legacy banking systems that are slow and expensive, Coinbax offers a middle path that satisfies both regulators and customers seeking speed.

Practical Applications: Real-World Use Cases

How does programmable escrow for stablecoin compliance actually benefit users?

- Cross-Border Payments: A business sending payroll to international contractors can settle in minutes instead of days, with all compliance checks handled automatically onchain. This benefits companies with global workforces.

- Interbank Settlements: Banks can transfer funds between each other using stablecoins while maintaining the same sanctions screening and identity verification required by regulators. This benefits financial institutions seeking operational efficiency.

- Treasury Management: Large corporations managing cash across multiple jurisdictions can use stablecoins for intra-company transfers without navigating different banking systems. This benefits corporate treasurers.

- Custody Services: Crypto custody firms can move client funds between hot and cold wallets with compliance controls built into the transaction flow. This benefits institutional investors.

- Wallet-to-Wallet Payments: As Glyman envisions, wallet addresses could eventually be associated with bank accounts, allowing seamless payments between bank customers and self-custody wallet users with compliance built in.

Risk Analysis: Expert Perspective

Primary Risks:

1. Smart Contract Vulnerabilities: Like all blockchain-based systems, Coinbax relies on smart contracts that could contain bugs or be exploited by hackers. A single vulnerability could lead to fund loss.

2. Regulatory Uncertainty: While MiCA provides guidance, global stablecoin regulation remains fragmented. What’s compliant in the EU may not satisfy US or Asian regulators.

3. Third-Party Dependency: Coinbax relies on external compliance service providers for identity checks and sanctions screening. If these services fail or provide inaccurate data, transactions could be incorrectly blocked.

4. Adoption Hurdles: Banks are famously slow to adopt new technology, especially when it involves moving funds. Gaining widespread institutional trust takes time.

Mitigation Strategies:

- Regular smart contract audits by independent security firms

- Multi-jurisdictional compliance frameworks that adapt to local regulations

- Redundant compliance service providers to ensure uptime

- Phased rollout with pilot programs before full-scale deployment

Expert Consensus: Industry experts agree that onchain compliance is the next frontier for stablecoin adoption. As one panelist at Consensus Miami noted, “Privacy and accountability can coexist onchain.” The challenge is implementation, not concept.

Beginner’s Corner: Quick Start Guide

If you’re a crypto user interested in how stablecoin compliance affects you, here are steps to understand:

1. Learn what stablecoins are: Start with USDC or USDT—these are the most widely used stablecoins that banks are integrating.

2. Understand smart contracts: These are automated programs on blockchains that execute when conditions are met. Coinbax uses them for escrow.

3. Check your wallet’s compliance: Some wallets now integrate compliance checks automatically. See if yours does.

4. Monitor regulatory developments: Follow MiCA implementation in the EU and potential US stablecoin legislation.

5. Watch for bank announcements: Major banks using stablecoins is a leading indicator of mainstream adoption.

Common mistakes to avoid:

- Assuming all stablecoins are created equal (each has different compliance standards)

- Ignoring tax implications (stablecoin transactions may trigger taxable events)

- Using non-compliant wallets for large transactions (risk of frozen funds)

Future Outlook: What’s Next

Coinbax’s roadmap points toward broader institutional integration. The company is already live on Base mainnet and running pilot programs—expected to expand to Ethereum mainnet and other Layer 2 solutions in the coming months.

Several trends will shape the future of stablecoin compliance:

- AI agent payments: As AI systems begin making autonomous payments, compliant onchain rails become essential

- Regulatory convergence: Global regulators are moving toward harmonized stablecoin standards, which will simplify compliance for companies like Coinbax

- Bank adoption acceleration: As more banks run successful pilot programs, expect rapid scaling of onchain compliance solutions

The vision Glyman described—where wallet addresses are associated with every bank account and compliance happens automatically onchain—could become reality within 3-5 years.

Key Takeaways

- Coinbax’s programmable escrow system solves the core compliance challenge that prevents banks from fully adopting stablecoins for payments

- Smart contracts handle identity checks, sanctions screening, and risk assessment automatically before funds settle onchain

- The system is already live on Base mainnet with pilot programs involving banks, custody firms, and wallet providers

- Onchain compliance represents the bridge between traditional finance and decentralized payments, enabling faster, cheaper transactions without sacrificing regulatory oversight

Stablecoin Yield Strategies: Low Risk Farming – A Comprehensive Guide

In the volatile world of cryptocurrency, stablecoins offer a safe harbor. But did you know you can earn consistent returns on your stablecoins without taking on excessive risk? This guide explores low-risk farming strategies that allow you to generate yield while preserving capital. Whether you’re a conservative investor or a DeFi newcomer, these methods can help you put your stablecoins to work.

Key Concepts

- Stablecoins: Cryptocurrencies pegged to a stable asset, like the US dollar (e.g., USDT, USDC, DAI). They minimize price volatility.

- Yield Farming: The practice of lending or staking crypto assets to earn rewards, often in the form of additional tokens or interest.

- Low-Risk Strategies: Approaches that prioritize capital preservation over high returns. Examples include lending on established platforms, providing liquidity to stablecoin pairs, and using insured protocols.

- APY (Annual Percentage Yield): The real rate of return, accounting for compounding interest. Lower APY often correlates with lower risk.

- Impermanent Loss: A risk in liquidity pools where the value of deposited assets changes relative to holding them. Stablecoin pairs minimize this risk.

Pro Tips

- Start with reputable, audited protocols like Aave, Compound, or Curve Finance.

- Diversify across multiple platforms to reduce platform-specific risk (e.g., smart contract bugs).

- Always check the insurance coverage of a protocol (e.g., Nexus Mutual) before depositing large sums.

- Monitor gas fees on Ethereum; consider using Layer 2 solutions like Arbitrum or Optimism for cheaper transactions.

- Reinvest your rewards periodically to compound your earnings, but factor in transaction costs.

FAQ Section

What is the safest way to earn yield on stablecoins?

The safest methods include lending on top-tier platforms like Aave or Compound, or providing liquidity to stablecoin-only pools on Curve. These protocols have been battle-tested and often have insurance options. Yields typically range from 2% to 8% APY.

Can I lose money with low-risk stablecoin farming?

While the risk is low, it is not zero. Risks include smart contract bugs, platform insolvency (e.g., a hack), or de-pegging of the stablecoin itself. Choosing established protocols and diversifying can mitigate these risks.

How do I start stablecoin yield farming?

First, acquire stablecoins (e.g., USDC) on a centralized exchange like Binance. Then, transfer them to a self-custodial wallet (e.g., MetaMask). Connect to a DeFi protocol, deposit your stablecoins, and start earning. Always start with a small test amount.

What are the best platforms for low-risk stablecoin yields?

Top platforms include Aave, Compound, Curve Finance (for stablecoin pools), and Yearn Finance (which automates strategies). For centralized options, consider Binance Earn or Coinbase Earn.

Conclusion

Low-risk stablecoin farming is an excellent way to generate passive income without exposing yourself to the wild price swings of the crypto market. By sticking to established protocols, diversifying your deposits, and staying informed about platform risks, you can earn consistent yields while keeping your capital safe. Start small, practice on platforms like Binance, and gradually scale up as you gain confidence.

For more details on this, check out our guide on Tax Loss Harvesting in Crypto: A Guide for Traders.

You might also be interested in reading about Identity on Chain: KYC and Compliance in DeFi.